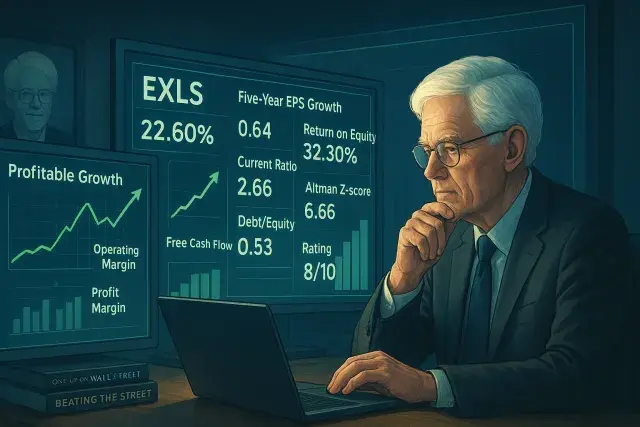

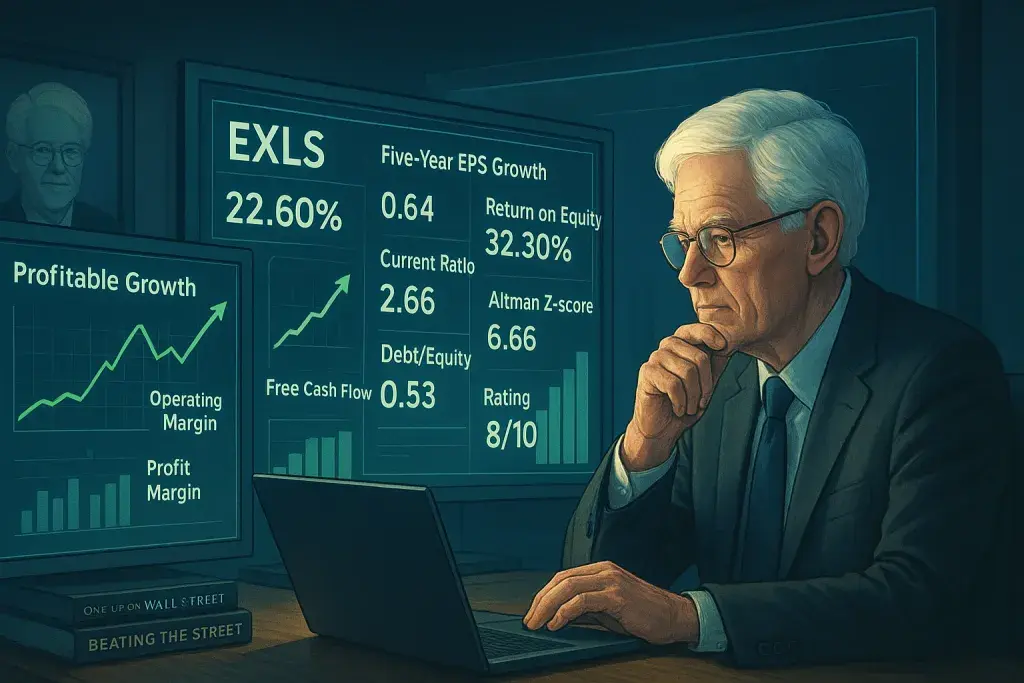

ExlService Holdings (NASDAQ: EXLS) has cleared every filter in a rigorous Peter Lynch-style investment screen, posting metrics that place it firmly in the "Growth at a Reasonable Price" category that Lynch made famous during his tenure at the Fidelity Magellan Fund. The company's five-year EPS growth rate of 22.60%, combined with a PEG ratio of 0.64 and a Return on Equity of 32.30%, tells a story of disciplined, compounding expansion that the market hasn't yet fully priced in. For GARP-oriented investors, that gap between demonstrated performance and current valuation is exactly the opening Lynch spent his career hunting.

What separates this kind of fundamental screen from a momentum trade is the insistence on financial health alongside growth. Lynch wasn't looking for hypergrowth at any cost - he wanted companies that could survive a bad quarter without breaking. ExlService's Current Ratio of 2.66 clears the minimum threshold of 1.0 by a wide margin, meaning short-term obligations are covered more than twice over. Its Debt/Equity ratio of 0.53 stays just under the screen's 0.60 ceiling. These aren't glamorous numbers, but they're the kind that keep a business running when credit tightens. It's worth drawing a parallel here to industries that operate under intense financial constraint - consider, for instance, how a cannabis dispensary pos maryland operator must manage cash flow and working capital with extreme care given limited banking access and the 280E tax burden, where maintaining liquidity ratios isn't a best practice but a survival mechanism.

The PEG ratio is where the Lynch methodology gets its sharpest edge. A PEG below 1.0 signals that the market is either ignoring the company's growth history or hasn't yet assigned it a premium valuation. ExlService's PEG of 0.64 is not marginal - it's a meaningful discount. Lynch's logic was straightforward: if a company has grown earnings at 22% annually for five years, and the stock's price-to-earnings multiple doesn't reflect that track record, something is mispriced. That's the opportunity. The screen isn't predicting future performance; it's identifying a historical pattern that the current price hasn't absorbed.

Profitability Metrics Reinforce the Core Thesis

An ROE of 32.30% is more than a checkbox. It indicates that management is generating strong returns on the equity it retains - not through financial engineering, and not by piling on debt, but through operational efficiency. The Lynch screen sets 15% as the floor; ExlService is more than double that. Combined with improving operating margins, profit margins, and gross margins over recent years, the profitability picture is consistent rather than episodic. That consistency matters. A single strong year can reflect a favorable environment. Several years of margin improvement suggests structural execution.

The Altman Z-score of 6.66 adds another layer of confidence. The Z-score is a multi-factor model designed to assess bankruptcy probability; scores above roughly 3.0 are generally considered safe territory. At 6.66, ExlService sits well clear of any financial distress zone. The price-to-free-cash-flow and EV/EBITDA figures cited in the full fundamental report further support the view that the stock is not overextended relative to peers. The full rating of 8 out of 10 - with top scores in profitability and financial health - reflects a company that isn't just growing but doing so from a stable base.

What the Screen Finds, and What It Doesn't Guarantee

Here's the catch: passing a Lynch-style screen is a starting point, not a conclusion. The screen identifies companies that fit a historical pattern of sustainable growth at a reasonable price. It doesn't account for competitive disruption, management changes, contract concentration risk, or macroeconomic shifts that could compress margins in future periods. Lynch himself was the first to say that knowing why you own a stock matters as much as knowing the numbers behind it.

The screen is also backward-looking by design. The 22.60% EPS growth figure reflects the past five years. Whether that rate persists, moderates, or accelerates depends on factors the screen cannot measure - client retention, pricing power, labor costs, and demand trends in ExlService's core business verticals. Investors running this kind of analysis should treat the output as a filter that narrows a large universe of stocks down to candidates worth deeper examination, not as a buy signal on its own.

That discipline - using quantitative screens to shortlist, then doing qualitative work to decide - is the actual lesson Lynch spent decades teaching. The numbers on ExlService are genuinely strong. The responsible move is to understand what's behind them before acting on them.

This article is for informational and educational purposes only and does not constitute investment advice. Always conduct your own analysis or consult with a licensed financial professional before making any investment decisions.